Your Business May Be Required to Offer a Retirement Plan

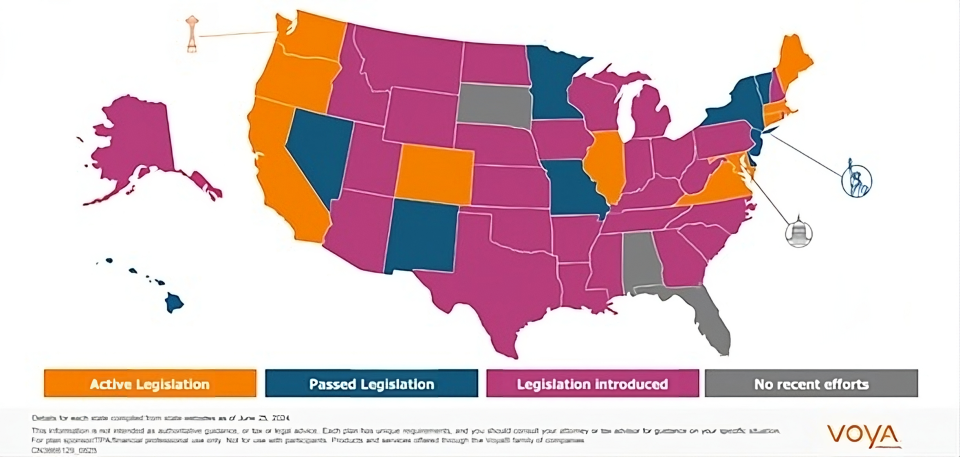

As of June 2024, 17 states, including California, Illinois, New York and New Jersey require businesses with more than five employees to offer a retirement plan benefit.

August 6, 2024

Guest post by Mitchell Haber, Regional Vice President (Los Angeles North - Emerging Markets), Voya Financial

With the number of states requiring businesses to offer retirement plan benefits to their employees on the rise, business owners should consider whether a retirement plan is a good option and, most importantly, find out if it is required in their state.

States that Require a Retirement Plan

As of June 2024, 17 states, including California, Illinois, New York and New Jersey require businesses with more than five employees to offer a retirement plan benefit, with 30 additional states considering state-mandated plans. Noncompliance can lead to fines of up to $250- $500 per employee per year.

Each of these states offers a government-run option, which can cost companies approximately one percent of the fees of plan assets to operate. With these plans, employees are currently limited to contributions of $7,000 to a Roth IRA per calendar year and automatically enrolled at a five percent contribution within 30 days of employment with the business.

Any of the following qualified employer-sponsored retirement plans would be acceptable in place of a state mandated option, but you still must register your exemption.

- 408(k) SEP Plan: Allows employers to contribute the lesser of 25% of an employee’s pay or $69,000 for 2024 to all employees over the age of 21, who have worked for at least three of the last five years for the employer and were compensated at least $750.

- 408(p) SIMPLE IRA Plan: Allows employees to contribute up to $16,000 in 2024 ($19,500 for employees over the age of 50). Employers must contribute 2% to all eligible employees or a matching contribution up to 3% of compensation.

- 401(k) Plan: Allows employees to contribute up to $23,000 in 2024 ($30,000 for employees over the age of 50) to either a pre-tax or Roth account. Employer contributions are optional but can be made up to an additional contribution of 25% of an employee’s salary capped at $43,500.

- Payroll deduction IRAs with automatic enrollment: Establishes an IRA (either a Traditional IRA or a Roth IRA) with a financial institution. The employee then authorizes a payroll deduction for the IRA. An employer’s responsibility is simply to transmit the employee's authorized deduction to the financial institution and should be offered to all employees.

Flexibility and Customization

Compared to other retirement plans, 401(k) plans offer flexibility and customization options. They allow businesses to tailor retirement plans, choose from various investment options, set contribution limits, and even offer employer-matching contributions to incentivize employee participation. In contrast, state-mandated plans have limited investment options and restrictive contribution limits, making it challenging to create a plan that aligns with some business goals.

Retirement Plan(s) Comparison Chart

|

|

Employee Contribution Limit |

Catchup Contribution for Employees 50+ |

Employer Contribution Limit |

Support for Pretax, Roth Tax Types |

Employer Match |

Vesting |

|

401(k) Plan |

$23,000 |

$7,500 |

$46,000 |

Both Pretax and Roth options |

Optional |

Various vesting schedule options |

|

SEP IRA |

NA |

NA |

25% capped at $69,000 |

Pretax only |

Mandatory |

Immediately |

|

Simple IRA |

$16,000 |

$3,500 |

$3,500 |

Pretax only |

Mandatory |

Immediately |

|

Payroll Deduction IRA |

$7,000 |

$1,000 |

NA |

Both Pretax and Roth options |

NA |

NA |

Portability and Employee Ownership

With a 401(k) plan, employees have full ownership and portability of their accounts, allowing them to take their retirement savings with them if they leave the company. This is a significant advantage over state-mandated plans, which often have withdrawal restrictions and may require employees to leave their funds behind if they change jobs.

Higher Contribution Limits

For example, 401(k) plans have significantly higher contribution limits than CalSavers, a California retirement plan program. In 2024, the annual contribution limit for 401(k) plans was $23,000 in both Pretax and Roth sources, while CalSavers has a limit of just $7,000 in after-tax Roth contributions.

Employer Matching and Tax Benefits

401(k) plans allow employers to make matching contributions, a powerful tool for attracting and retaining top talent in the competitive music products industry. Additionally, employer contributions are tax-deductible, providing a valuable tax benefit for your business. On the other hand, state-run retirement plans do not offer employer-matching contributions, and contributions happen with after-tax dollars.

Professional Management and Support

With a 401(k) plan, employers can access professional management and support from a third-party administrator and financial advisor, ensuring that your plan complies with the Employee Retirement Security Act (ERISA) and Department of Labor regulations and providing guidance on plan administration.

Tax Credits Offset the Cost of Administration and Offer Free Employer Matching to Employees

Starting a 401(k) plan can be costly, but the tax credit helps offset these expenses, making it more affordable for small businesses like music retailers. With government tax credits, most companies can offer a 401(k) with no out-of-pocket costs for the first three years.

Businesses can also get government tax credits to give their employees up to $1,000 of employer matching for each of the first five years you offer a retirement plan. The government pays your employees and covers the cost of creating these programs.